At the end of April, the UK Financial Conduct Authority announced that it intends to extend its Sustainability Disclosure Requirements (SDR) and investment labels regime to all forms of portfolio management services.

The decision would bring the rules for portfolio managers more closely in line with those for asset managers. It would include model portfolios, customized portfolios and bespoke portfolio management services.

The financial watchdog argued that by extending the requirements to portfolio managers it would help improve consumer trust, market integrity and minimize greenwashing.

Its consultation closes on June 14 and it plans to publish the final rules in the second half of the year.

What are the proposed rules?

Firstly, if a portfolio manager is making no sustainability claims, then it faces no new requirements. However, under the FCA’s proposed rules, it would then be forbidden from making any claims alluding to sustainability, ESG or positive impact.

If a portfolio manager wants to make sustainability claims, then it must apply to the FCA for one of four labels. These labels depend on the portfolio’s sustainability objective. Further, to use a label at least 70% of the overall portfolio arrangement would need to be invested in accordance with this sustainability objective.

The portfolio’s assets must be selected with reference to a “robust, evidence-based standard” that is an “absolute measure of environmental and/or social sustainability”. It must also have key performance indicators that demonstrate progress towards achieving the sustainability objective.

The four investment labels proposed by the FCA.

If a portfolio manager does not want to apply for one of these labels but still claim that its services have sustainability characteristics, it must produce the same types of disclosures as required for labelled products. It will also have to produce a statement clarifying the reason why it does not have a label.

A portfolio manager that does not want one of the FCA’s labels also cannot use “sustainable, sustainability, impact and any variation of those terms” in any of its communications.

Overseas funds remain out of the scope of the SDR and labelling regime. However, the Treasury have announced their intention to consult on extending the regime to overseas recognized funds.

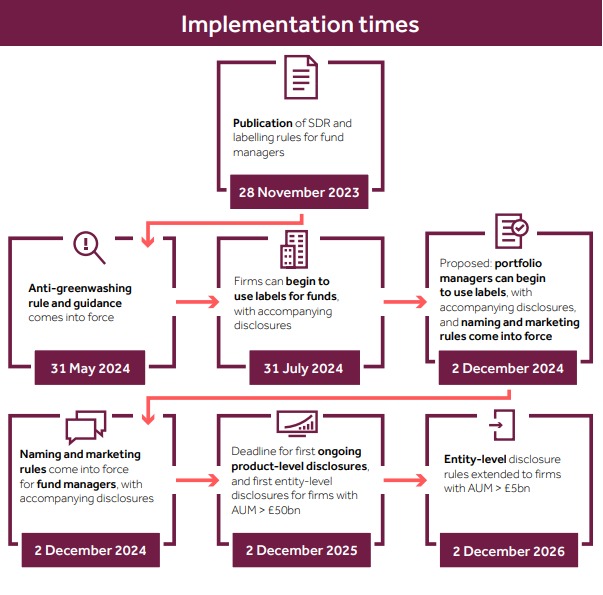

When would this come into force?

The FCA proposes that the labelling, naming and marketing requirements, and their associated consumer-facing and pre-contractual disclosures, will come into force on December 2, 2024. Product-level disclosures are expected to follow a year later.

Firms with assets under management greater than £50 billion will need to produce entity-level disclosures by December 2, 2025. Meanwhile, firms with AUM greater than £5 billion will have until the same date in 2026.

The FCA said this follows a similar approach to the final rules for fund managers.

The FCA’s proposed timeline for SDR